Sleep Number (SNBR)

The question is not if, but when!

Sleep Number is a direct-to-consumer (DTC) specialty mattress company that has consistently been highly profitable with strong margins over the years.

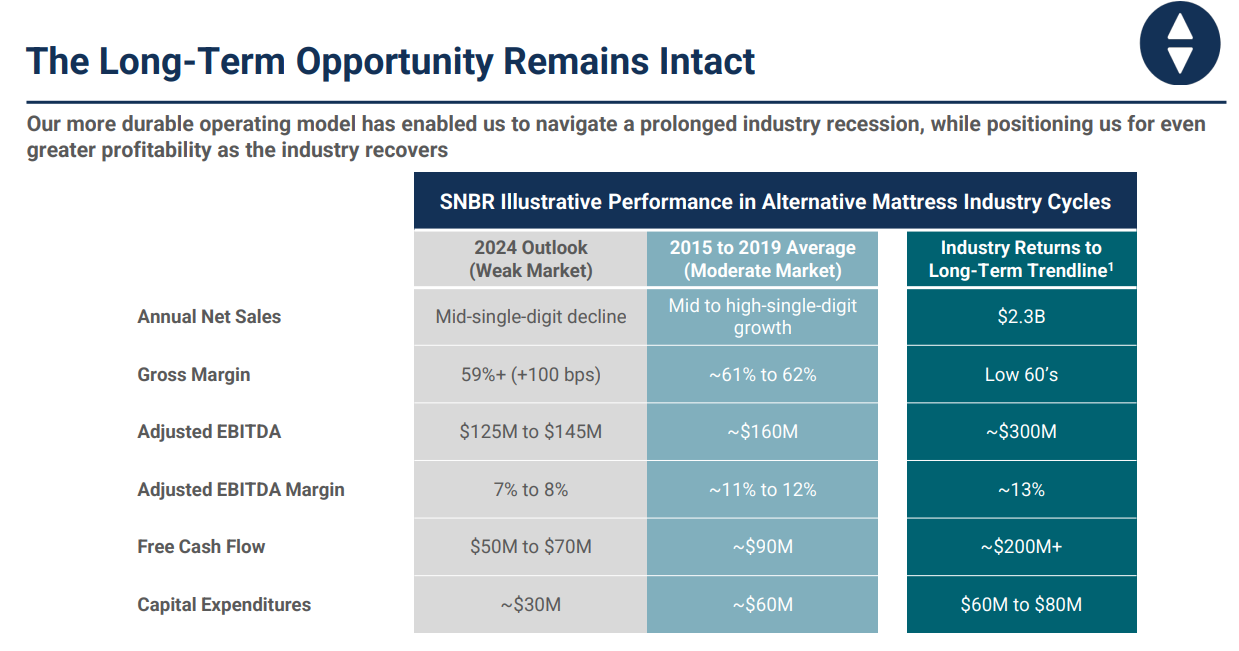

Despite the overall mattress industry volume in 2024 being below 2015 levels, Sleep Number has generated $50 million in free cash flow YTD even while carrying a significant amount of debt.

I believe the equity is currently trading at 2–3 times normalized mid-cycle earnings, offering the potential for multiple-fold returns when the cycle inevitably turns.

Company Description - Market Breakdown

The total U.S. mattress market can be broken down as follows:

65% inner spring beds

25% foam

10% specialty

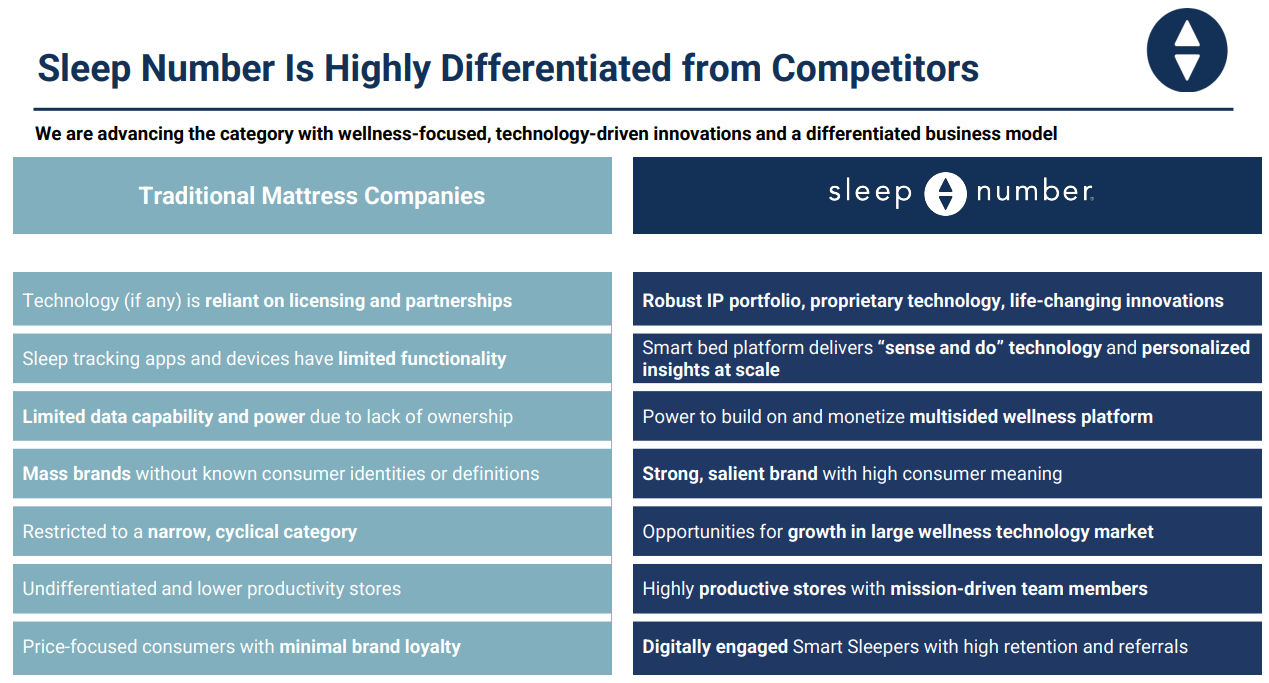

Sleep Number is the largest player in the 10% specialty segment of the market, with an estimated 12%–15% market share and the most profitable.

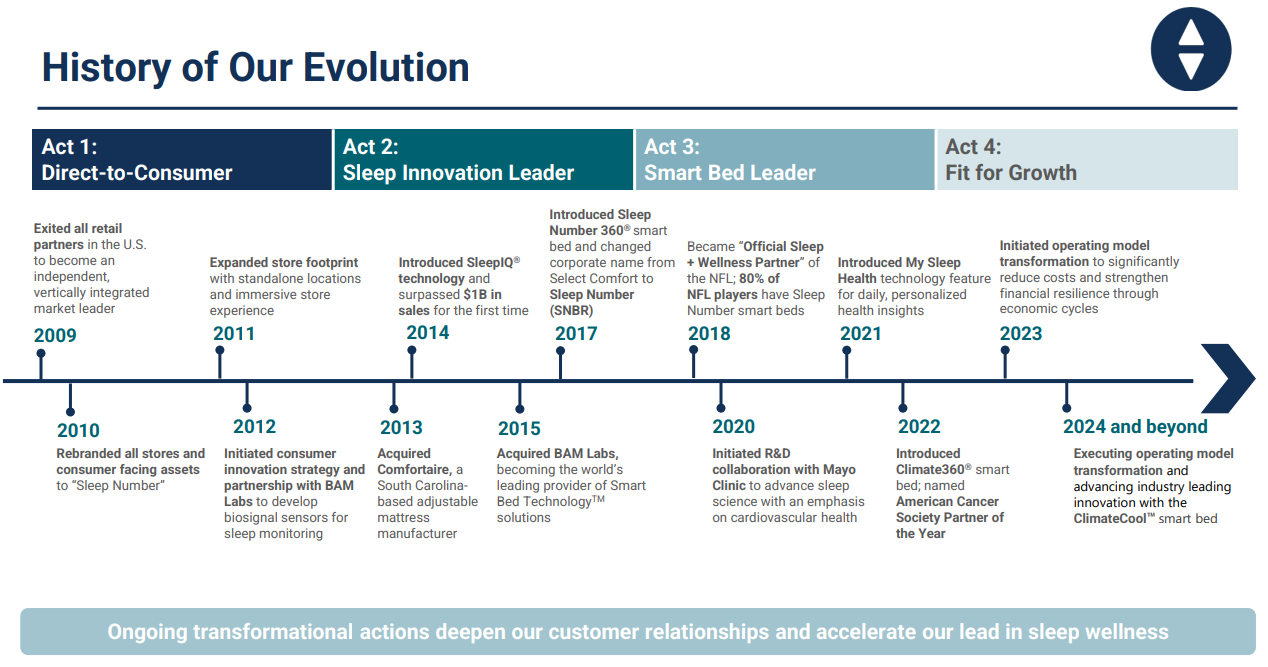

They have built their position over the years through several strategic approaches:

Direct-to-consumer retail model:

This allows them to avoid being commoditized in large retail selections.

Continuous innovation in their offerings:

They are well-known for their SleepIQ score and personalized sleep experience.

Customer-Centric Retail Experience: For example, they pay salaries and commissions to floor salespeople, ensuring that employees are not entirely incentivized to pressure customers (which is not the industry norm).

Significant investment in national advertising:

Over the years, they have spent millions on national campaigns, including their famous NFL ads. As a result, most people in the U.S. are likely familiar with the brand.

All these decisions have led to a strong market position within its segment, enabling the company to achieve gross profit margins of over 60%.

Current Mattress Market

According to both LEG and TPX, mattress units in 2024 are expected to be down in the high single digits compared to 2023. That would put the industry units at between 2015 and 2014 volumes. The market appears to have bottomed out, with some growth expected in 2025.

Industry Turnover Cycles

In the mattress industry, mattresses typically have a turnover cycle of 7 to 8 years. This means that much of the volume purchased over the last five years will likely require renewal in the next few years.

Demand is not disappearing permanently; consumers are delaying purchasing a new $5K–$10K bed. Additionally, mattress demand is closely tied to new home purchases, which have recently seen some recovery.

Valuation

Shares Outstanding: 22M

Long-Term Debt: $516M

Lease Liabilities: $352M

Stock Price: $14

Equity Value: $308M

Enterprise Value (EV): $1.2B

Adjusted EBITDA 2024: $115M–$125M

Free Cash Flow YTD: $50M

The stock appears incredibly undervalued—there’s no need to overcomplicate it.

Assuming a return to 2019 unit volumes as a reference for the mid-cycle earnings power of the business. In 2019, the company generated $1.7 billion in revenue and $81.8M in net income, a net margin of approximately 4.8%. With 28M shares outstanding, EPS of $2.70.

Assuming the same revenue level and 4.8% margin, plus a $60M reduction in costs, net income would be $141M. With only 22M shares outstanding, that’s EPS of $6.40 for a stock currently trading at $14.

Historically, the market has valued this business at 15x–20x forward earnings.

Notably, 2019 wasn’t a particularly strong year, as shown in historical performance data. Moreover, the average ticket size has increased significantly due to inflation.

One could argue that the business and brand are stronger today than they were in the pre-COVID era. The company has invested millions in advertising over the past few years, and its overall footprint is larger than in 2019, although its store count has contracted from its peak in 2023 (2019: 611 stores, 2023: 672 stores, today: 643 stores).

The company has likely achieved cost reductions closer to $100 million. Management has set a target of $130 million in operating expense savings compared to 2022, to be realized across 2023 and 2024. This year alone, they have achieved $44 million in savings. Additionally, gross margins have improved from approximately 55% in 2019 to around 60% in 2024, driven by value engineering initiatives.

Debt Considerations

The company carries significant debt on its balance sheet, which is relatively expensive. Despite this, it generated over $50M in free cash flow (after interest and CapEx) YTD during a year when industry volumes were below 2015 levels.

However, covenants kicking in next year are a potential concern. The company needs to maintain leverage below 4x starting in Q1 2025. Management believes they can meet this requirement with revenue of $1.7 billion. If the bottom falls out, the company could face challenges. That said, a supportive banking group and a potential backstop from large shareholders could help address any near-term liquidity needs.

If the company returns to any type of growth, this could become a home run investment!

Recent Developments

The company announced in Q3 that their long-time Chairman and CEO, Shelly Ibach, is retiring. This is the same CEO who, in 2021–2022, spent $427M to buy back 4.9M shares at an average price of $87, leaving the business in a precarious position for the coming years and resulting in a stock price decline of over 90%.

While Shelly Ibach deserves credit for the business's operational achievements, she was a terrible steward and allocator of capital.

Stadium Capital, the largest shareholder, has consistently bought shares over the past few weeks. On 11/25, they issued a letter arguing that they must be more involved in the new CEO hire, as the old board cannot be trusted: Letter Reference.

The CEO’s retirement is a bullish development. For many investors following the business, the outgoing CEO was one of the largest overhangs. The new CEO has not been announced yet. Still, regardless, they would inherit a fundamentally strong business that is coming out of a difficult period and hopefully returning to growth in 2025.

Risks

Covenants: If market conditions worsen in 2025, the company might struggle to meet its debt covenants. While I don’t believe there is significant bankruptcy risk, the company could face dilution in that scenario.

New CEO: The identity and vision of the new CEO remain unknown, which introduces uncertainty.

Recession Risk: A severe, demand-driven recession could significantly impact the business. However, one could argue that the last two years have already been such a period.

Summary

I believe Sleep Number is an above-average cyclical business that is currently trading significantly undervalued compared to its normalized earnings power. When the cycle turns, I think this stock has multi-bagger potential.

Although there are some uncertainties, I believe it might be the right time to invest in an inexpensive, leveraged cyclical business as we approach 2025.